Executive Briefing|August 22, 2019

Is Defined Contribution Coming to Healthcare?

Share:

Will new trends drive defined contribution and a new consumer choice model?

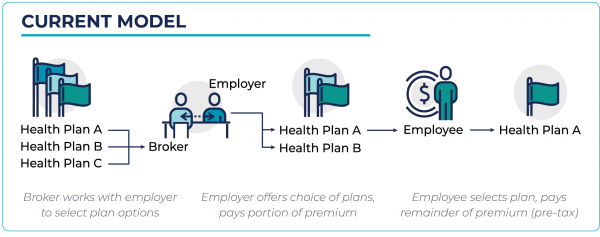

Just as the employer retirement market shifted from defined benefit to defined contribution (such as a 401k or 403b) nearly 25-years ago, the employer group health insurance market may be poised to make a similar shift. Will the recent ruling-making related to health reimbursement accounts (HRAs) change employers’ group purchasing decisions?

This recent rule issued on June 13, 2019 by the Department of Health and Human Services, Department of Treasury, and Department of Labor in response to a 2017 Executive Order (13813), “Promoting Healthcare Choice and Competition Across the U.S.” allows employers greater flexibility to offer an “Individual Coverage HRA” as an alternative to traditional group health coverage. The ruling also created a new, limited type of HRA called an “Excepted Benefit HRA” that can be offered in addition to a traditional group health plan.

Individual Coverage HRA | Excepted Benefit HRA |

|---|---|

|

|

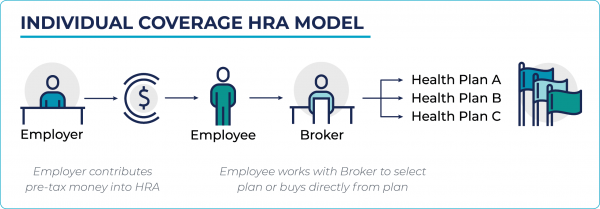

We believe it will take time for employers to digest and change their benefits strategy; however, we believe that the rule highlights an industry-wide shift towards enhanced consumer choice and engagement. Similar to the Medicare Advantage market (MA), in which individuals shop for plans with various levels of coverage and enroll directly through a plan or broker, increased adoption of individual coverage HRAs could shift the employer market towards this model. This paradigm shift will create an imperative for health plans to evaluate their strategies for consumer and provider engagement in order to be successful in this new environment.

STAKEHOLDER IMPACT

Stakeholders will experience a mixed impact with some positive and some negative implications as this rule is implemented over the next few years and based on the approach employers take with the ruling. We also expect variation on a market to market basis; as such, stakeholders should carefully consider their local market dynamics as they formulate strategies related to this rule.

| STAKEHOLDER | POSITIVE | NEGATIVE | DEPENDENCIES |

|---|---|---|---|

| Consumers | Potential to provide more transparency, better choice, and ability to keep plans over their lifetime | Potential to burden consumers with decision making and higher cost sharing if plan contributions do not meet the cost of buying insurance | Dependent on individual market adoption and whether individual plan options offer better pricing, coverage, and benefits than the employer group market |

| Employers | Creates more options and flexibility for coverage, relief for employers facing acute cost issues, and greater transparency into health benefits as an employee retention / acquisition lever | Could be perceived negatively by some employees leading to abrasion | Ability to leverage as a strategy to retain and attract talent will be market and industry driven |

| Health Plans | Creates a vehicle to increase individual market penetration while simultaneously stabilizing the membership risk pool | Most plans do not have the membership acquisition and retention strategies in place necessary to be successful with a large individual market book; in addition, many plans do not yet achieve margin potential in this space, compared to other books of business | Dependent on whether plan has experience in individual market and is prepared to compete on consumer-centric qualities and price, as well as better manage the risk of an individual market pool |

| Brokers | Creates another avenue for discussion with employer clients and enhances individual market opportunities in the long-term (e.g., brokers play a large role in Medicare Advantage) | Forces brokers to shift from a B2B model to direct collaboration with consumers, which will require a different set of core competencies | Dependent on broker experience with consumer centric sales |

WHAT ARE THE ADOPTION EXPECTATIONS?

Individual coverage HRAs create short-term relief for employers facing acute cost pressure and flexibility via new coverage options. Employers’ adoption of the rule will depend on several factors, including:

Factors Accelerating Adoption | Factors Limiting Adoption |

|---|---|

|

|

|

|

| |

|

Initial government estimates project that it will take five years for employers to adjust to these new rules; after which, approximately 800,000 employers will choose to offer Individual Coverage HRAs to pay for insurance for more than 11 million employees and family members. As a result, between 2020 and 2029, individual coverage is expected to increase while traditional group enrollment will decline. This projected shift in membership does not drastically change the employer market, representing less than 1% of overall employer coverage; however, if this trend moves up market into larger employers or is combined with new regulation / legislation, this HRA rule could mark the start of a transformative approach to employer-based coverage.

Although it is tempting to take a “wait and see approach” given the nominal immediate impact, plans must be mindful of the broader factors driving the rule which must be addressed regardless of the rule’s moderate adoption:

- Affordability: Healthcare costs continue to rise and healthcare is becoming increasingly unaffordable for many employers, with limited ability to shift these costs onto their employees

- Consumer Choice: Developing strategies that attract and then engage members will become increasingly important. Once enrolled, activating employees in their health to improve navigation and care management programs should be a critical goal of these types of individual plans in future years

- Employee Lifecycle: Building a lifetime understanding of members who shift products (e.g., commercial to Medicare) or shift employers will become increasingly important as consumers begin to have more choice in their health insurance options

- Integrated Cost of Care Management: Creating a proactive and integrated approach to managing care of members who could be longer tenure will pay off on plan MLR strategies

WHAT ACTIONS SHOULD HEALTH PLANS TAKE?

Focus on Affordability: In the individual coverage paradigm, affordability, as measured by premiums, will be critical to driving membership growth. Health plans must continue their efforts towards addressing the broader coverage affordability issue, recognizing that utilization and pricing can only be addressed through greater influence in the market with aligned provider partners. Such alignment can be achieved through strategic, value-based partnerships or ownership of providers and clinics.

Align Product Strategy to Better Support Consumer Choice: Product strategy must also support this provider alignment. Specifically, the traditional, broad network PPO will not support actions needed by providers to effectively manage the cost of their assigned, attributed populations. The individual choice structure will likely drive HMO adoption. While some employer and/or market dynamics will continue to favor broad PPOs, over time many employers, facing cost pressures, will offer alternative products alongside a traditional PPO offering. This shift is expected to occur due to premium differential and superior member experience.

Improve Consumer Engagement to Retain Members Throughout Their Lifecycle: Health plans must develop and execute on strategies to better attract and acquire individual group members similar to Medicare Advantage. This requires investments in marketing, lead generation, and retention strategies that are different from a direct to group model.

Increase Integrated Care Management: Integrating care management across physical, behavioral, pharmaceutical, and social / lifestyle factors will be critical to managing a fully insured population with a longer expected tenure.

Begin to take action on these four objectives by taking a few key next steps:

NEXT STEPS

Evaluate local market dynamics

Determine whether your market will support an accelerated adoption of new individual coverage options. Consider:

- Richness of State Exchange (e.g., number of carriers / products, average premium)

- Employer segmentation by size, industry and geography

Develop communication and outreach strategy

Target employers most likely to be impacted by the recent rule-making. Consider:

- Timing

- Tailor to employer circumstances and decision-making criteria

Evaluate individual market strategy

Determine if any changes are needed to address rule-making impacts. Consider:

- Product design

- Benefit design

- Pricing

Continue to evaluate and advance strategic initiatives

Focus on addressing root cause issues related to cost trend and affordability. Consider:

- Value-based contracting / provider partnerships

- Provider / clinic ownership

- Systems of care / care management support

- Consumer engagement and activation strategies

- Community health partnerships and social barrier identification

- Data / analytics / reporting to support desired outcomes related to cost and quality

- Product and benefit design

HEALTHSCAPE CAN HELP.

We have experience evaluating local market dynamics to help our clients stay ahead of key market and regulatory events. Contact Jesse Owdom at (804) 513-4741 or jowdom@healthscape.com for more information.