Executive Briefing|September 7, 2017

Industry Perspectives on Value-Based Payment: Survey Results & Key Insights

Share:

HealthScape Advisors recently partnered with the Health Plan Alliance and several of our health plan clients to survey plans about their experiences, approaches and performance under value-based payment models. In doing so, HealthScape surveyed over 30 health plans through a standardized questionnaire and follow-up executive interviews to more deeply understand each organization’s journey towards value-based care and supporting fee-for-value payment models.

Our survey of health plans focused on the following key areas:

- Perspectives on value-based payment models and drivers of success

- Common themes and distinctions across market segments and products

- Effectiveness of health plan operating models in supporting execution

- Differences in performance between provider-sponsored health plans (PSPs) and traditional health plans (Non-PSPs)

The insights we collected reflect an industry in transition. Our survey results demonstrate a wide variety of approaches, reported successes and challenges in driving affordability and quality outcomes through value-based payment models.

The shift to value-based payment is a slow one, with most plans not yet making the transition to risk.

Of plans surveyed, the majority (60%) indicated that pay-for-performance or upside-only shared savings arrangements were the most prevalent value-based payment models (VBPM) in their portfolio.

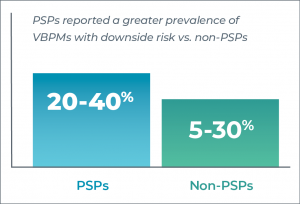

Survey results indicate that provider-sponsored plans (PSPs) may be a bit further along in shifting financial risk to providers. Between 20-40% of PSPs surveyed indicated that a VBPM with downside risk is the most prevalent model for a particular line of business, compared to 5-30% of non-PSPs. We also noted differences among lines of business. Risk assumption was highest in the fully insured group line of business via upside and downside shared savings/risk and in Medicare Advantage via a mixture of shared risk and capitation.

Scale and health plan market share are critical to drive provider engagement.

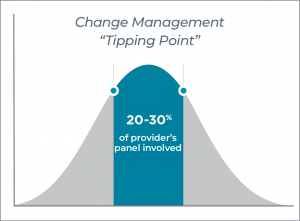

For a provider practice to justify the capital investment (both human and financial), a sufficient portion of its patient panel must be involved in the value-based payment model.

We typically see an increase in provider commitment and engagement occur once 25-30% of a provider’s panel is involved and/or assuming risk in value-based payment arrangements. This change management “tipping point” creates a challenge for smaller plans, which often do not have the required “wallet share” of their provider partners. Of the health plans that report over 25% “wallet share” with their network providers, the majority (53%) of these plans report positive outcomes in quality and cost. However, for the plans representing less than 25% wallet share, only 36% report positive quality and cost outcomes. Of note, most PSPs surveyed report that they represent less than 25% of their providers’ panels.

While provider integration or alignment is a prerequisite, it does not guarantee improved performance in VBPMs (and differences are noted between PSPs/non-PSPs).

This result suggests that provider integration is a requirement for success; however, it does not guarantee success by itself. Despite reporting tighter integration with providers, PSPs do not necessarily report greater success in quality and cost outcomes than non-PSPs. Generally, PSPs reported lower rates of achievement in quality and cost of care outcomes. For example, only 30% of PSPs surveyed reported success in both quality and cost of care outcomes, as compared to 60% of non-PSPs reporting improvements on both measures.

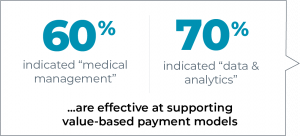

Transformation capabilities within care management, data management & analytics are viewed as critical drivers of success under value-based payment models.

Our survey revealed that both capabilities correlated highly with reported success in value-based payment models. For the plans reporting success and effectiveness in the care transformation function, we noted a wide variation in approaches. We also observed the commonality of many PSPs leveraging their unique and strategic relationship with their provider owners in the deployment of their care management tactics and interventions.

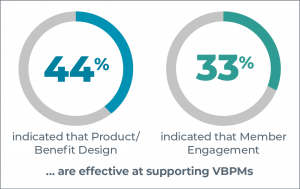

Product alignment & member engagement are missing enablers across the industry.

Nearly all health plans report low effectiveness of product and member engagement compared to the other core capabilities that are critical toward successful execution under value-based payment models. For example, only 44% and 33% of surveyed health plans reported that product/benefit design and member engagement, respectively, are effective in supporting value-based payment models.

HEALTHSCAPE RECOMMENDATIONS

Take advantage of inherent strengths or build care transformation capabilities and data-driven insights to create value in VBPMs

PSPs may have an inherent structural advantage for these capabilities, which can help to overcome the wallet share challenges noted previously. However, recent partnership ventures between providers and non-PSPs are seeking to replicate this structural advantage and use scale to drive interest in these VBPMs. Continued focus must be on collaboration with providers for bi-directional information sharing and delineation of roles and responsibilities between the provider and health plan to help advance VBPM success.

Improve consumer engagement through enhanced product benefit design and consumer navigation support

Both product/benefit design and member engagement are critical levers; yet, up to this point, they have been underutilized by health plans to support value-based payment models. Value-based benefit design without adequate member engagement through both clinical and financial navigation has not led to significant savings. Accordingly, enhancements in product design can help support VBPMs in achieving desired cost and quality outcomes by lowering financial barriers that could prevent patient adherence or management of their conditions (e.g., free primary care visits, no copays for maintenance drugs/supplies). The recent Oscar Health + Cleveland Clinic partnership represents an innovative model that will use multiple platforms to drive consumer engagement, including dedicated concierge teams and internet-based self-navigation.

Accelerate the roadmap to risk by aligning with government models and strengthening financial alignment with primary care physicians and specialists

It is often said that “timing is everything” and this adage may be especially apt given the significant change in provider reimbursement represented by MACRA. Health plans can capitalize on the disruption created by this legislation and should work to align the structure of VBPMs with the parameters outlined by MACRA. While timing may be delayed, it is recognized that the FFS model is fiscally unsustainable and MACRA may also help accelerate providers’ willingness to accept risk. Accordingly, health plans should look for opportunities to migrate existing models to include risk assumption or create new models that meet required risk thresholds.

HEALTHSCAPE CAN HELP.

The financial transition to a pay-for-performance model can be challenging, but HealthScape can help. We are experts in assisting our clients recognize their provider integration and value-based capabilities. For more information, contact Alexis Levy at (312) 256-8671 or alevy@healthscape.com.

About the Health Plan Alliance

The Health Plan Alliance is a national organization that brings provider-sponsored and independently-owned health plans together with their health system and provider group leaders for unparalleled peer-to-peer collaboration. Alliance member health plans are well represented across various stages of development and all lines of business with an emphasis on Medicare, Medicaid and Commercial. For more than 20 years, Health Plan Alliance members have leveraged the collective knowledge of our community to enhance their business acumen and advance the quality of health care delivery in their communities. For more information visit healthplanalliance.org or email info@healthplanalliance.org.